When I was in the insurance line (for only half a year), I once was talking to a fellow colleague (“A”) who mentioned about his conversation with his friend (“B”). With a tone as if he was full of knowledge, he said that when he knew B paid his housing loan quickly whenever he got extra cash and soon after, cleared his housing debt, he scolded B. A said that rather than paying his housing in full in the shortest possible time, he should use that money to invest somewhere, such as making a deposit for another house. Using the concept of leverage, he could have made even more money in the long run.

You may have heard of this kind of story many times, by people who made it in life, by people who gave financial advice, by people who may have certain knowledge in this. The main purpose of this article is not to condemn or promote the use of leverage, but to highlight the risks and rewards that come with it. If used well, this can potentially be the path for you to climb up the financial ladder. If used wrongly, it can sink you and your whole family.

Investopedia defines leverage as:

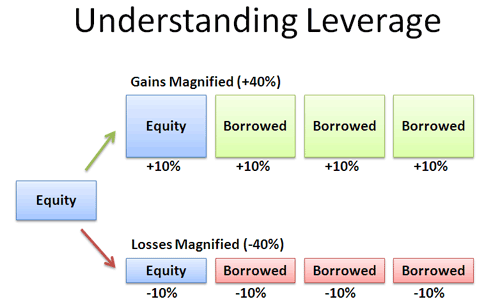

Basically, with the $1 you have, you borrow for example $10 for investment, trading, purchases etc. This applies in the stock market, forex trading, crypto futures trading, housing market etc. With leverage, your profits are magnified, giving you potentially great profits with little capital, allowing you to earn multiples of your initial capital within a very short period of time. On the other hand, it is the same for your losses. If not done well, you will lose your initial capital far quicker than you expected. A simple diagram below illustrates this:

Today we will discuss on using leverage for housing, something that affects most of us.

Using a simple example (figures vary between countries but the concept is more important): I have $300,000 now. 1 house cost $300,000. The deposit for a house is $50,000, with an interest rate of 3% per year.

On one end I could put $300,000 down and pay for 1 house in full. I will owe no debt and have no need to pay for any interests. From young we were taught not to owe any debt, pay off any outstanding as quickly as possible or the interests will sap our wealth. Paying for interests is like throwing money into the drain. That logic itself is no wrong. In fact, I would even say it is correct to teach children this concept.

On the other hand, instead of paying $300,000 for a house, I will buy 6 houses, each with a deposit of $50,000. I will then be owing the bank a total of $250,000 x 6 = $1.5 million.

That seems like a daunting bill. But if I break it down using a very simple calculation, it will mean that per house:

Cost of 1 house – $300,000

Deposit – $50,000

Interest payment – $250,000 x 3% = $7500 a year.

20 year housing loan – $250,000 / 20 = $12,500 payment per year

Housing loan payment + interests – $12,500 + $7500 = $20,000

Per house I need to take out $20,000 a year to pay off what I owe.

However, since I am the owner of the 6 houses now, I can stay in 1 house as originally planned, and rent out the other 5. All I need to do is to rent out the house at about $2500 per month = $30,000 per year. Now my situation is this:

Annual repayment amount – $20,000 as calculated above

Rental income – $30,000 as calculated above

Earnings per year, per house – $10,000

With that, my tenants are effectively paying my housing loan and interests for me! Not only that, I will have some additional profit which can be slowly used to offset the initial deposit I paid for the houses, or to simply pay for the very house I am staying in and thus not rented out to generate income. As an additional benefit, if the housing price goes up, I can even sell it off at a higher price.

The above example is a very classic and typical one of using leverage. On theory it seems very plausible and effective way to do things. Of course, the above example talks about 2 extreme ends. Most of us do not choose to act in an extreme manner. I could buy only 2 houses or 3 houses instead of stretching myself to the limit of 6 (based on the given example’s financial power).

However, when we get down to it, there are a few issues to take note of. Personally, I have used leverage to get my second house, but that is because my situation gave me the confidence that I could get it sorted out. I did not go for a third house even though I could. More will be explained later.

First, your credit score must be good. If your credit score is bad, nobody will be willing to lend money to you. Remember to get your credit card early and pay your credit card bills in time (this portion differs in different countries). If you do not have a good credit score, you will not be able to borrow as much as you wish to. While the above example gave the illustration to borrow and stretch to 6 houses, practically speaking for many of us, 2 houses is the limit. If your credit score suffers and you are not able to borrow as much, you will not be able to even enter the game of leverage.

Second, your main source of funds. While on paper it seems easy to just buy house and rent it out, chances are your earnings may not be as high as you calculated it to be. Maybe some of the houses will be empty for some time. Some of the houses need additional cost to renovate. There are taxes to be paid. Stretch yourself too thin, and you will find yourself having difficult to pay for the loan and the fees. For example, what if you lose your job suddenly? Will you still be able to pay the housing loan if you stretched yourself too thin? Getting fired, retrenched, company not renewing your contracts etc are very common things which happened to many people. That is not to say you should not play with leverage. But when using leverage, do consider if you will still be able to sustain if you lost your main source of income.

Thirdly, what will happen if you die? If you are alone, then maybe everything will go to waste. But if you are married, your debts will become your spouse’s debts. If both of you are going through this together, you will need to figure out what happens if one of you is gone for good. Will the other be able to pay off the loan? That is where insurance came in. I bought insurance, so that if I die, all my debts will be paid off immediately, cutting off all financial burden.

Fourth, the value of the house. If you know how to think of using leverage, there are a thousand others who also know how to use it. In a hot property market, prices are sky high. People are confident and optimistic about the future, as it is with everyone just before a crash. Of course one may say that the housing price has been going up for the past 5, 7 or 9 years. Even the financial crisis which was supposed to come in 2018 or 2019 did not come, and everything just went sky high. I am no economics expert, but do take note that if you bought at a high price using leverage, and suffer an economic downturn where property prices dropped, you will still be stuck paying for the mortgage for a highly priced house when the actual value is already a fraction of before.

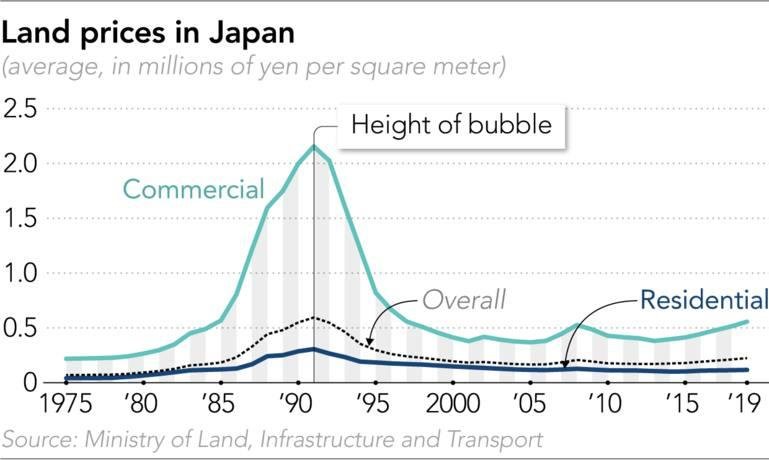

Using a real life example, one of the factors causing Japan’s lost decade came from the fourth point. While there are complex economic theories behind it, I will talk about the property aspect part. Japan’s property prices were getting higher by the day, and the banks were giving out loans at a very low interest rate without regard for the quality of the borrowers. This sparked the idea of leverage in many people. People put down a minimal deposit, and borrowed the rest of the amount. Property prices went further up as people snatched up real estates everywhere, believing that with the capital appreciation they would earn huge amounts of money which they would not be able to with a normal salaried job. This causes an inflationary bubble way beyond what the country could handle. To counter this, the Bank of Japan raised interest rates sharply, causing the bubble to burst.

Why would the bubble burst? If you stretched yourself to the limit, you are essentially trapping yourself, giving yourself no leeway for any changes. In this extreme situation where everybody is buying house (and hence nobody really needs to rent), you would not earn much from rental income. What is really supporting your housing loan is your salary only. If you are already stretching yourself to the limit with a 3% interest rate, then you would collapse if the rate went up from 3% to 4%. Everybody around you will fall into a debt they could not pay and be forced to sell their houses cheaply. But since everyone is doing that, property prices will plunge. Japan increased their official discount rate (basically interest rates which the central bank lends to the commercial banks) from 2.5% in 1989 to 6% in 1990. What happened is that equity plunged 60% by 1992, and land values fell 70% by 2001. Imagine the number of people who went bankrupt.

Taking this further in today’s context in China and elsewhere in the world, there are countries all over trying to clamp down the housing price and diminish the asset bubble. On top of what was explained above, if everybody is speculating in real estate and driving up the prices, people would start giving up what they are supposed to do. Factories will pump money into real estate instead of manufacturing goods, farmers would buy properties instead of doing actual farming which is hard labour but yield little. Salaried workers will not work as hard as they feel their day job pays too little. This leads to a serious problem – an economic whose foundation of agriculture (food) and production (actual goods) are eroded but things as fluff as real estate (way over the basic needs of 1 house per household) becomes the main economy’s driving force. When things collapse and housing prices are no longer appealing, the country would have nothing left but a financial bankrupted population. At this time, other countries will swarm in with their money to buy over critical resources of the country. US is always doing that.

In Chinese, we have a saying: 水能載舟,亦能覆舟.

The literal translation goes: Water can carry a boat, and also capsize a boat.

This is the same for leverage. If you are just stepping into the world of leverage, start small. Do your homework. Even if you have all the head knowledge and are well-versed in the theory, start small when practically trying it out. There will always be unforeseen circumstances, or even circumstances which you would and should have expected but could not react in time or react well when things actually happened. Do not be greedy and go big early on when you tasted some early and quick success. But be patient, be disciplined, try it out over a period of time. Then see if it is suitable for you. See if you are able to take the stress and sleep well at night.

I have tried leverage playing futures in the crypto world and found myself losing sleep at night, frequently checking on my phone for the latest price movements etc. I am in fear of liquidation, and in fear of not taking profit quickly enough even though I set stop loss and take profit queues. I decided that in the end, although I do leverage for my house purchase, I could not do well in the futures market. I decided to stop it, and now only play the crypto spot market.

Leverage is a tool. Some use it well, some do not. Some use it well in certain areas, but not in others. Test it (if need be) and know yourself whether you are suitable or not. If you are not suitable for it, there are many other ways to earn money. The path to success is many, and so are the tools. You do not need to know how to use every tool well. You just need to be proficient in the tool you are able to use well.

So the next time you hear someone scolding someone for not using leverage, or come across someone advising another to use leverage, know that everybody is different. Everyone’s characters, situation and goals are different. Just so you know, most people giving financial advice in a personal or even professional capacity are not even good at managing their finances themselves. Do your own homework about the type of leverage you are to play, and do homework on the overall economical and political climate.

Showing 1 - 3 out of 3

Page 1 out of 1

| - | Shop Products | Price | |

|---|---|---|---|

|

|

|

$99,999.00

|

|

|

|

|

$1.00

|

|

|

|

|

Price range: $69.00 through $99.00

|

It is an interesting concept to be able to leverage one thing against another, financially. I don’t think I would have the financial knowledge to strategize. It is good to learn about how this works.

Leverage can be an interesting and useful tool! Thank you for explaining it so well!

It is really nice to learn about Leverage and aspects of it. It was an interesting read! Thank you.

Finances can get so complicated, that was a lot of information on just one aspect of it. Impressive! And thank you for sharing the insight!

This blog on “Leverage” is an eye-opener, highlighting the power of utilizing resources effectively.

This information about leverage is important to know. You explained it very well.

Your article on leveraging in housing is insightful and practical. You’ve provided a balanced view of the risks and rewards. It’s a valuable guide for readers to make informed decisions about their financial future. Great job!

I need to work on sending in a bit of extra money to my mortgage company. My house will be paid off in 8 years but I’d like it paid off sooner if possible. I will have less income once my son graduates and having a house that is paid off will greatly reduce my expenses.

This is all really good to know. I usually have a hard time understanding this kind of stuff, but you explained it really well.

Thanks for the explanation! While I understand the appeal and potential gains involved with leveraging, the idea scares me a bit. I don’t like going to far out on a ledge.

As I read your post, I really understood what leverage was. Thanks for sharing this with us.

You explained this really well. I admit I didn’t know much about leverage.