In certain societies, climbing up from the bottom class to the middle class may be a difficult but realistic target. Achieving good academic results and going on to getting a decent job would be the default route. However in most societies, it is extremely difficult for the middle class to save for their first pot of gold. People generally remain a slave their whole lives.

Limited Working Days

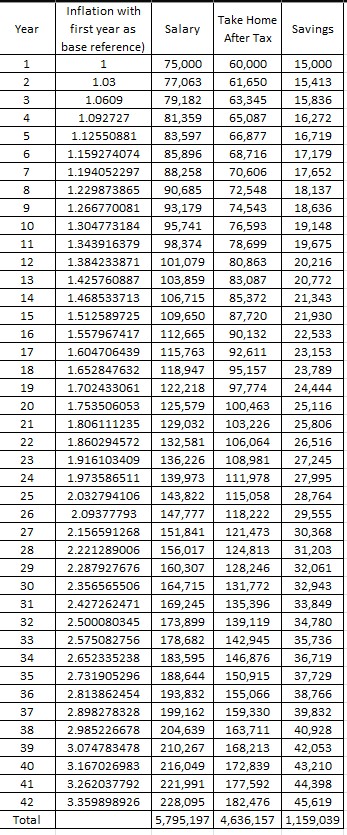

Using Singapore as an example, we assume the average student graduates from the university at 23 and retire at 65. There is about 42 working years. For men, that is even lesser because Singaporean men need to serve 2 years of military conscription. Using today’s market rate, we assume a fresh graduate earning about $5000 a month ($75,000 a year including a 3 month bonus) and ending his career at $15,000 a month ($225,000 a year).

Under such a circumstance, this salaryman will be earning about $5.8 million over the course of his lifetime. Assume a 10% income tax rate and a further 10% forced savings by the government (in Singapore, we pay 20% for CPF but part of it can be used to buy our houses, so I will take that out), we have a 20% deduction from our salary, bringing our take-home income over a 42-year period to approximately 4.6 million.

This is the maximum income a middle class person can have over his lifetime. We know this is on the ideal side because we assumed no gaps in employment (ie retrenchment) and that the person’s salary increases every year till he retires. In actual reality, this is too good a picture for most.

Inflation

Most governments would like to market their inflation as around 2-3%. However realistically, we know it is more than that. One mass money printing during the Covid era simply made things minimally 50% more expensive over a 5-year period.

Again we assume an inflation rate aligned with the government data of around 2.5%, the middle ground. Over a 42-year period, a $1 item would become (1.025)^41 = 2.75. This means that your first year of savings would have eroded to about 1/3 of its original value, though this erosion gets lesser as you get closer to the present time.

We assume a savings rate of 20%, in terms of raw numbers alone the salaryman would have saved 1.16m over his lifetime. However, with an inflation at 2.75 since he started working, his actual purchasing power from his total savings would only be 1.16m / 2.75 = $421,800 in his younger days. Adding whatever amount from his government retirement funds (do note that we have taken this into consideration by assuming a 10% CPF instead of 20% deduction), this has to last him till he dies because we would not want to be working at 90.

With a starting salary of $75,000 per year and ending salary of $225,000 a year, one will work out a salary increment of 2.75% per year, barely outrunning the inflation. On the surface it looks like I am advancing, but in actual reality I have never moved away from my original spot.

Purchasing Power

Taxes are stackable. Take alcohol for example, we have the import duties and the GST. With my taxed income, I will pay for a double-taxed beer. What about cars? Properties? A average salaryman’s purchasing power is reduced layer by layer by the different open and hidden taxes that in the end, most people find it hard to save even 20% of their salary.

Conclusion

Not everyone can be at the top of the pyramid. Any society will require the bottom class to deliver their pizza and the middle class to be their corporate slave. And the system is designed to ensure things run in order. But with enough discipline, financial literacy and good planning, the first pot of gold can still be achieved in good time.

在一些社會,從底層爬到中產階級是個困難但能實現的目標。努力讀書,畢業找份好工作即可。但在大多數社會,要存下第一桶金,是非常艱難的。大多數的人一輩子都逃不出奴隸的命運。

有限的工作日

以新加坡為例,假設一個學生23歲大學畢業,65退休。這就是42年的工作時間。因為新加坡男人得服2年兵役,所以工齡是更少的。以當今的市場勞動價為準,可假設大學畢業生月薪5000(包含3個月花紅是年薪75000), 退休時達到月薪15000(年薪225000)。

在這個狀況下,這打工人一生能賺580萬。再假設10%個人所得稅和多10%強制儲存(在新加坡,大家付20%公積金,但部分錢可用來買房,所以這裡簡單計算),薪水就扣了20%,拿回家的只有460萬。

這是一個普通中產這一生的上限。而我們知道這是往好的方面想,因為我們又假設了就業沒有空擋(裁員),加上這人的薪水都是每年在增長,直到退休為止。

通脹

很多政府都會說他們的通脹在2-3%之間。但實際上我們知道通脹遠超出這個數字。疫情間的大印錢就讓物價在5年內漲超過50%。

我們取官方通脹的中間值,2.5%。42年後,一個一塊錢的東西將會變成(1.025)^41 = 2.75. 這代表了你第一年存的錢會貶值到原來的1/3,雖這個貶值會隨著越接近現在時間越少。我們再假設一個人能成功的把20%的薪水存下來,這一生他能存下116萬。但當通脹達到2.75,他的購買力將會變成他出社會時的 116萬/2.75 = 42.1萬。加上退休後能拿出的公積金(註:這我們早前已經考慮到了,所以公積金的計算是按10%而不是20%計算),這筆錢得維持到他生命的終點。畢竟誰都不想做工做到死。

起薪7.5萬,退休時達到22.5萬的薪水,這就是一年漲薪2.75%,勉強跑過通脹。看似有進步,實則原地踏步。

購買力

稅是層層疊加的。拿酒做例子,我們有進口稅和消費稅。拿著我被稅的收入,我再去買被稅2次的酒。車呢?房呢?一個普通打工人的購買力通過各種公開和隱藏的稅被層層剝削。到最後,又有幾個人能存下20%的收入呢?

總結

不是每個人能在金字塔的頂端。任何社會都需要底層人送你的外賣,中產來做牛馬。而這系統,就是為此而設計。但只要足夠自律,有足夠的財商和計劃,第一桶金還是能存到的。

Showing 1 - 3 out of 3

Page 1 out of 1

| - | Shop Products | Price | |

|---|---|---|---|

|

|

|

$99,999.00

|

|

|

|

|

$1.00

|

|

|

|

|

Price range: $69.00 through $99.00

|